08 Oct Backdating Farm Depreciation Tax Credits

One of the most frequent questions that I am asked by clients is “Can I still have a depreciation report completed on a farm I purchased numerous years ago?”.

The only limit to how far back you go is simply one of economics. The law sets time limits for amending your tax assessment. For individuals and small businesses, the time limit is generally two years, and for other taxpayers four years. Depending on which situation above you fall under, then you are unable to claim the depreciation from the last year that your accountant can amend for you back to the purchase date of the property. The other factor that will influence the economic outcome is the depreciation method that you choose.

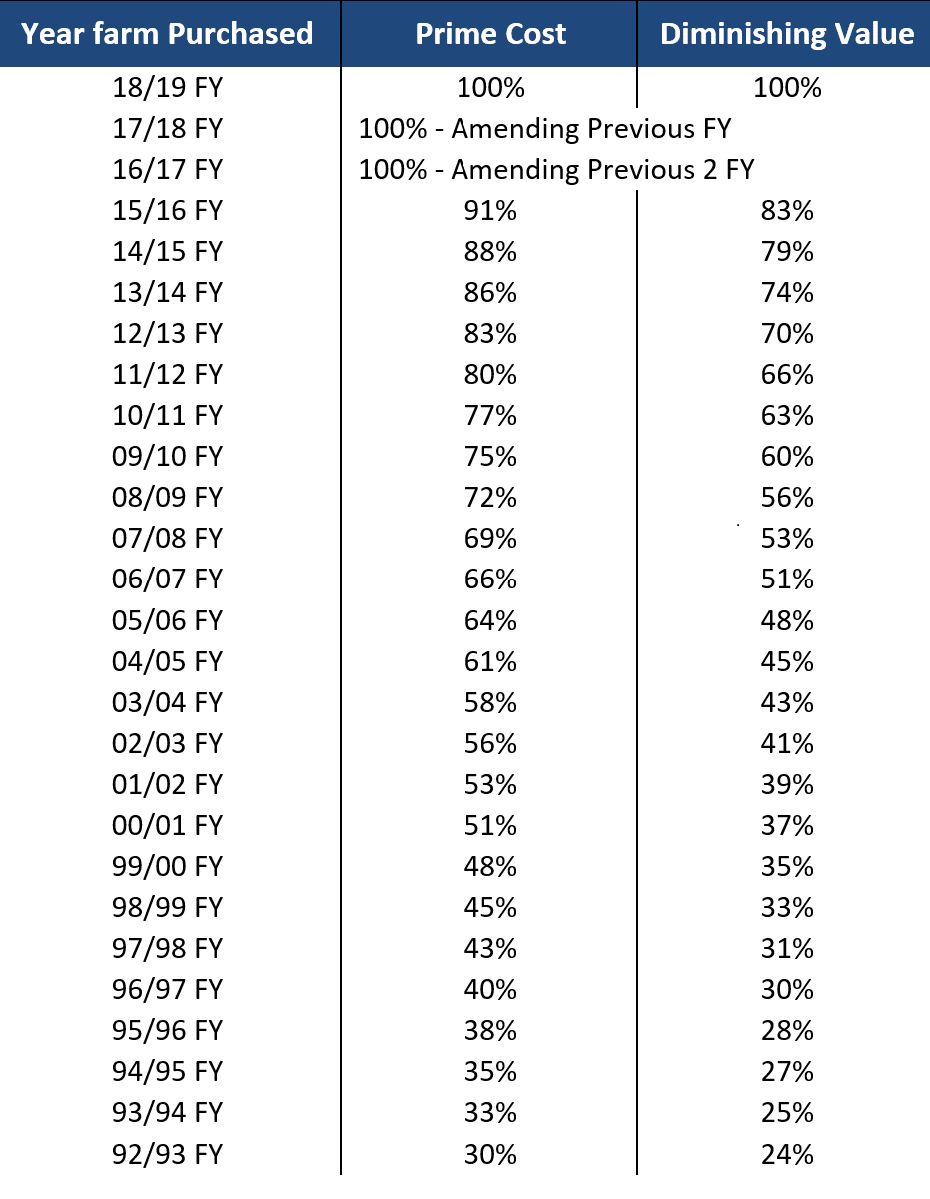

The table below shows a case study that was completed which estimates the potential depreciation still available to be claimed based on a report being completed before lodging 18/19 Financial Year tax return.

Robinson Sewell Depreciation (RSD) has an extensive data-set of farms that allows us to provide an estimate of the potential depreciation that may be available. We then work with your accountant to ascertain if it is economically beneficial to have a farm depreciation report completed on a property that you purchased in the past.

Sorry, the comment form is closed at this time.