12 Aug 0% Borrowing Rates

Conceptually you could buy large farming aggregations, industrial warehouses, portfolios of commercial property and blue-chip waterfronts. Without interest to pay, there is no opportunity cost of capital. Theoretically, the servicing test would be non-existent, and the pain of liability would fade into dinner party discussions of what life used to be like burdened with debt.

The Dawn of a New Era

Photo taken near Harden, NSW

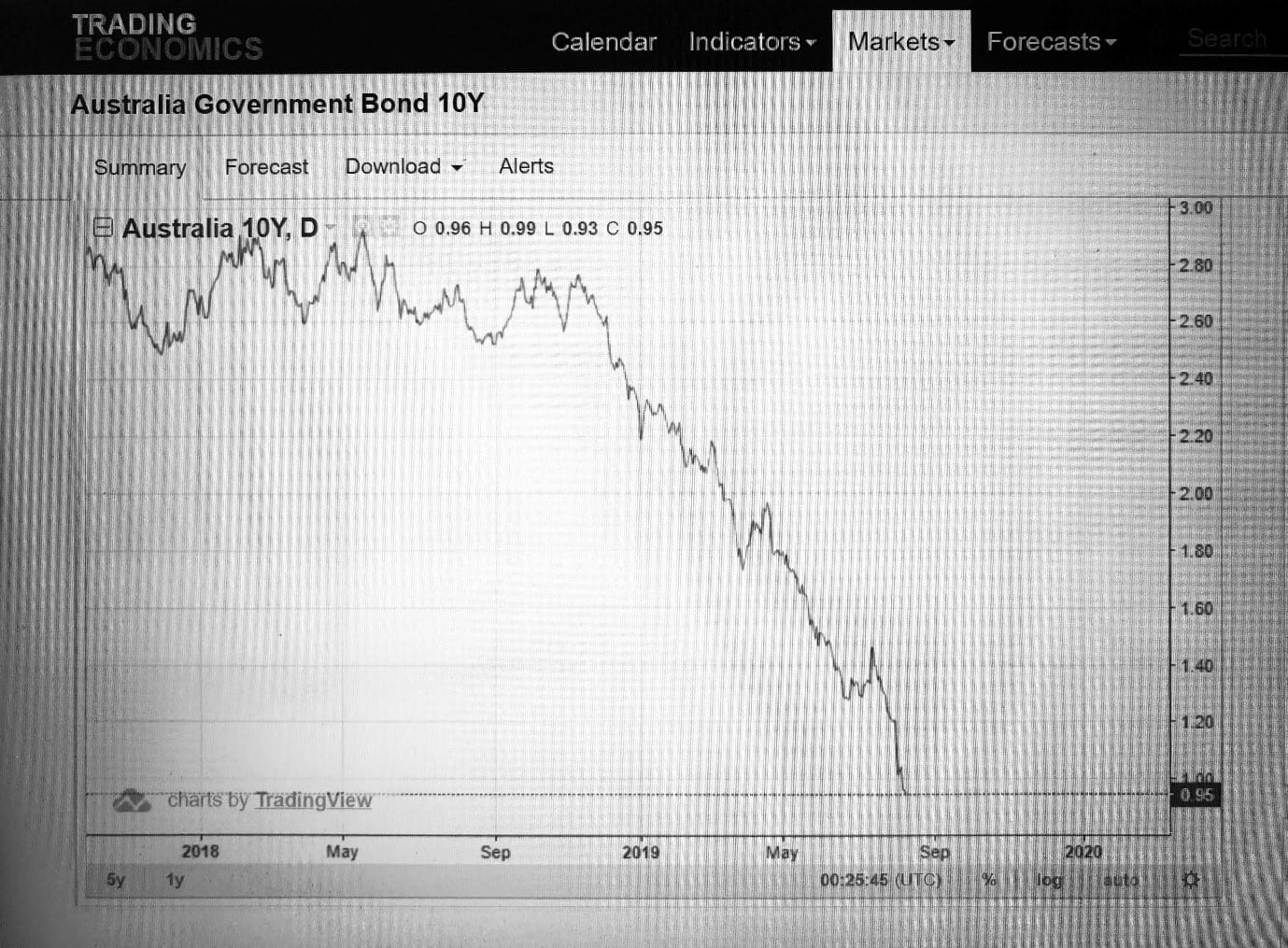

As of last Friday, the Australian 10-year bonds were trading at 5 points discount to the RBA overnight cash rate of 1.00%. This meant that the Australian government could borrow money for 10 years at a cost of only 0.95% p.a. With the current inflation rate in Australia is 1.3% p.a. this means, in actual terms, the real borrowing rate for the Australian government is -0.35%.

10 Year Bond Yields “Falling off the Cliff”. Source: tradingeconomics.com

There are already 25 countries trading with their official rates being 0% or negative. The rush to invest in Australian AAA bonds is quickly pushing our rates to a similar calling, and further projections of RBA rate cuts supports this supposition.

Long term rates are driven by sentiment, tenure risk and inflationary expectations. Interest rates that are pushing towards negative territory means one fundamental conclusion: the inflation rate is falling and is projected to continue to do so. With the demand for money falling below that of supply, the medium-term prognosis for Australia’s welfare is not healthy for inflation Keynesianism’s believers.

Land values can decline in a deflationary environment

In simple terms we are talking about deflation. The price attained for an asset tomorrow will be lower than that of today. This monetary dynamic naturally defers investment and expenditure and hence creates a self-perpetuating environment of falling employment and general economic welfare. Why would anyone pay for an asset today when it will be cheaper tomorrow?

Even though Australia’s current inflation figure is 1.3%, this was calculated on a rolling historical basis. The 10-year bond yield curve is a quasi-predictor of future inflation. And it is here where analysis derails the monetary status quo that asset prices will continue to rise over time and an acquisition of a primary assets today will be worth more in the future.

The mathematics of 0% borrowing rates

For the retail borrower who wants to buy the farm, the commercial property or the waterfront home, here are some hard truths if you find yourself accessing funds at 0%.

First, on average, the big four banks achieve a Net Interest Margin of about 2.00%. This means the banks make a profit of 2.00% over their cost of funds.

Banking 101: who wins and who loses

If the banks begin lending at 0%, it means that their cost of funds has fallen to -2.00%. In very crude terms you will be seeing Term Deposits being offered at -2.00%, interbank lending (swaps) trading at minus 2.00% and the RBA cash rate being deep in negative territory.

It will also most likely mean that deflation has now gripped the country, and real asset prices have begun to fall across the board. The property you just purchased will be worth less in 12 months’ time and so on.

So, buying primary assets like real estate, the cash flow generation maybe positive, but there will be a capital loss accumulating on the balance sheet from the deflationary effects of the overarching macro environment.

How to Borrow when rates are 0.00%

Assuming the funds are to purchase a primary asset, the two key underlying principles still need to be applied;

- The current and projected security position.

- Reliability of servicing.

The cash flow generated on the borrowing must now exceed the rate of deflation (compensated by principle debt reduction) noting that the security position will erode over time.

Plus, the investment must then generate a satisfactory risk adjusted Return on Investment (ROI) over and above the deflation compensation payments. Remember cash flow and cash flow certainty too can diminish over time in a deflationary environment.

A paradigm shift in mindset needs to be applied to rationalising investment profiles and decision making agenda’s.

Conclusion

Borrowing at 0% is not a free kick to society. It can create a serious social burden with severe implications to income generation (especially for retirees). A majority of (sub optimal) investments that are sub consciously made on emotional bias will no longer be compensated and diluted by the supporting effects of asset inflation.

Business decisions and investment will need to be more aligned to rational analysis and strict risk management guidelines.

Be happy and content that we pay interest on our borrowings, the world in which we don’t may not be that rosy.

Sorry, the comment form is closed at this time.