19 Jun Farm Tax Depreciation Benefits: The Untold Story

Story by Michael Stout, Robinson Sewell Partners

Take home message

- If you have purchased a farm in the past 10 years or more, or a farm has been transferred into another entity, you may be sitting on thousands of dollars’ worth of tax deductions.

Background

With agriculture being so buoyant across the country over the last few years for both farming families and corporate agricultural investors, appetite to acquire farms has been strong. During this investment phase, one major consideration has been missed which could have huge tax advantages for the purchaser. Potentially between 10-30% (and sometimes more) of the purchase price could consist of infrastructure assets that can be depreciated to offset future taxable income. The good news is, past acquisitions can be back dated.

Discussion

When a farm is acquired, the land value and infrastructure assets make up the total price on the contract of sale. It is important from a tax standpoint to allocate value to depreciable infrastructure items and set those items within an ATO compliant depreciation schedule beginning with the tax year in which possession is obtained. Of course, land is not depreciable, but when a farm is acquired, there will be infrastructure assets on the land that are depreciable such as fences, buildings, yards, silos, tanks and dwellings.

To increase the ATO compliance outcome with the value ascribed to these assets, the ATO recognises Quantity Surveyors as having the appropriate qualifications and skills to estimate the construction costs for use in depreciation reports. A Quantity Surveyor is an expert in construction costs and are recognised in accordance with ATO tax ruling 97/25 by the Australian Taxation Office as the most suitably qualified profession to estimate the depreciable expenditure spent on the improvements, plant and equipment prior to your purchase. Even if it was constructed 25 years ago a Quantity Surveyor can estimate cost using historical data and therefore increasing your depreciation entitlements. Your Accountant is unable to do this for you, however, what a Quantity Surveyor can do will positively enhance and maximise what your Accountant can produce. Effectively a Quantity Surveyor compliments the services of your accountant.

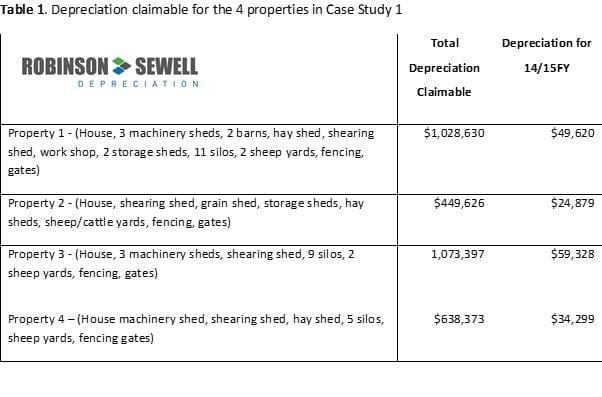

CASE STUDY 1

A rural farming family in the Riverina

After four strong seasons had exhausted all their previous tax losses that they had incurred from a run of dry years. They were now in a position where their business was very profitable and they were looking for a tax effective ways to reduce their tax liability.

As they had purchased some farms over the last several years their accountant suggested that they speak to Robinson Sewell Depreciation (RSD) about depreciation schedules for the assets that came with the farms.

In February 2016 RSD conducted an in-depth inspection of all assets on the farms that they had acquired. This included houses, machinery sheds, shearing sheds, barns, silos, grain sheds, sheep/cattle yards, fences and gates.

From the farm inspection, RSD’s specialized agribusiness quantity surveyor then compiled valuations on each of the assets and provided a tax schedule for each property which was ATO compliant. The total depreciation that could be claimed over the “effective life” of the assets was $3,190,026 with $167,826 claimable as depreciation for the 14/15 financial year which they were about to lodge.

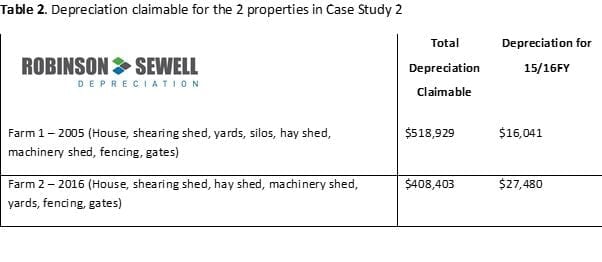

CASE STUDY 2

A family in the Bathurst region running a fat lamb and wool enterprise.

With strong wool and lamb prices the family purchased a farm in 2016 to add to their existing farm that they purchased in 2005 and the original family farm. They were recommended to have a farm depreciation report complied on the property that they had just purchased. RSD’s preliminary analysis and due diligence uncovered that not only would it be beneficial to have a report done on the new property, but it would also be beneficial for the property that they purchased in 2005. RSD carried out a thorough inspection of both properties and a ATO compliant report was compiled by their specialized agribusiness quantity surveyor.

Further Details with Farm 1 which was purchased in 2005.

The client’s accountant could amend their previous two financial years which reflected an additional $34,647 depreciation claimable. The client was unable to claim depreciation between 2005-2013 but still had the total benefit remaining of $337,797 over the effective life of the assets.

Conclusion

- Depreciation tax benefits can potentially be back dated 2-4 years;

- Acquisition and family succession property transfer can potentially trigger the benefits;

- Has been beneficial for clients to complete depreciation schedules on properties purchased more than 10 years ago;

- Depreciation schedules completed by qualified agribusiness quantity surveyor specialists; underpin the creditability of ATO compliance.

Contact details

Robinson Sewell Partners

PO Box 7353, Wagga Wagga NSW 2650

0427 692 418

[email protected]

@MichaelStout

Sorry, the comment form is closed at this time.